Court Record Data Shows Enduring Harm from Private Student Loan Default Judgments

on Topics: Case Research | Future Law | Perspectives

Court data is a necessary ingredient for meaningfully gauging the scope of the growing access to justice gap in the United States and is a critical tool for advocates seeking to close the gap through legislative action.

To highlight ways in which court data can be used to inform and evaluate legislative and regulatory reforms, UniCourt is featuring a three-part series of guest blog posts from Claire Johnson Raba on her work to improve access to justice for self-represented litigants in state courts.

In her first guest post, Court Data Access Drives Legislative Change: A Story From California, Claire shared examples from California on how court records data can help legislators understand the magnitude and scope of the issues low-income people experience when interacting with the court system. Claire concluded her first post by noting that “the value of analyzing court record data to identify problems means that the success and efficacy of legislative change is measurable and the bills that work to improve access to justice and fair outcomes can be replicated in other states, backed up by research that shows what works.”

Claire’s second guest post digs deeper into the data from her report, Co-opting California Courts: How Private Creditors Have Turned the Judiciary into a Predatory Student Debt Collection Machine, and details how private student loans disproportionately burden borrowers of color, how private student loan borrowers fare poorly in court, certain steps California should take to protect borrowers, and much more.

Court Record Data Shows Enduring Harm from Private Student Loan Default Judgments

Private student loans can haunt borrowers for decades after they leave school, standing in the way of economic stability. When borrowers miss payments on their loans, state court lawsuits are often filed by lenders or debt collectors to collect delinquent student loans, creating a barrier for low-income borrowers trying to climb out of debt. A report analyzing court data from California, Co-opting California Courts: How Private Collectors Have Turned the Judiciary into a Predatory Student Debt Collection Machine, shows how debt collection lawsuits filed in state court to collect private student loans often end up rubber stamped, giving lenders the right to get paid from the wages and bank accounts of low-income workers. In California, judgments accrue interest at a rate of 10 percent per year and are renewable every ten years, effectively making them enforceable indefinitely.

Private Student Loans Pose Risks for Borrowers

There are two types of student loans: federal student loans and private student loans. Federal student loans are backed by the federal government and payments are collected by servicers hired by the Department of Education. When borrowers fail to pay, the Department of the Treasury can garnish a borrower’s income and levy a borrower’s bank accounts using administrative processes. Low-income borrowers unable to pay their federal student loans have options to avoid default, such as income-based repayment programs that allow them to keep their loans in good standing while adjusting payments to an affordable amount each month. Federal loans can be taken out of default through consolidation or rehabilitation. Federal student loans may also be eligible for discharge under programs like the recently overhauled Public Student Loan Forgiveness Program for borrowers who work in public service jobs, total permanent disability discharges, and closed school discharges.

Private student loans have historically been marketed to student borrowers who attend for-profit schools, such as trade schools. Although many of these schools lost their accreditation and are out of business, thousands of borrowers still owe on loans taken out to finance high-cost, low-return degrees earned from disgraced and bankrupt schools like the ITT Technical Institute, DeVry, and the Corinthian Colleges: Everest, Heald, and WyoTech.

Private student loans, originated by private lenders, are riskier and do not come with the same protections for borrowers. They also often have high interest rates – sometimes in the double digits – and are coupled with extremely long repayment periods. This results in an extraordinarily high cost of credit. Private student loans also require a credit check, so family members often end up co-signing for these loans, placing parents and grandparents on the hook if the borrower defaults.

Private student loans begin to accrue interest immediately, while the borrower is still in school, and when the borrower graduates or stops attending school, the loan immediately comes due (in contrast to federal loans, which have a grace period). When borrowers are unable to make their payments, servicers may place borrowers into forbearance, or in temporary reduced-interest payment plan where interest continues to accrue and is added to the balance of the loan at the end of each year through a process known as income capitalization. Over time, borrowers often end up paying more in interest than the amount borrowed in the first place.

Private Student Loans Disproportionately Burden Borrowers of Color

The burden of private student loan debt is not equally distributed across student borrowers. The Student Borrower Protection Center found that while Black borrowers are half as likely to take out private student loans as their white classmates, Black borrowers with private student loans face nearly four times higher than the rate of delinquency by white borrowers. Twenty-four percent of Black borrowers of private student loans have fallen behind on payments, compared to less than 7 percent of white borrowers. The disparate impact of these predatory and high-cost student loans on communities of color and Black borrowers counters the argument that education is “the great equalizer.” In the face of a racial wealth gap in which the net worth of a typical white household is ten times that of a Black family, private student loans end up harming the most vulnerable borrowers and their communities.

Private Student Loan Creditors Take Borrowers Behind on Payments to Court

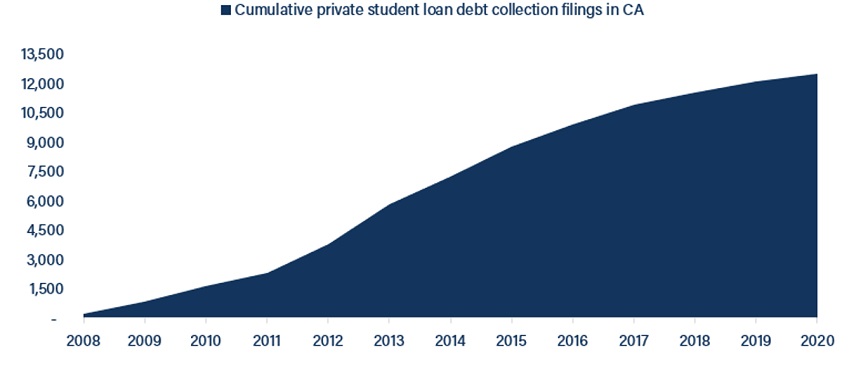

In California, an estimated 650,000 borrowers owe over $10 billion in private student loans. Not all borrowers default on their loans, but when they do, these debts often end up in court. In an analysis of twelve years of court records, my study found that student loan borrowers were sued in more than 12,500 lawsuits across California. Most of these lawsuits are brought by student loan debt collectors that represent statutory trusts – legal entities that bought up hundreds of thousands of private student loans that then sold notes secured by the loans to investors. Many of the creditor plaintiffs have confusing names like National Collegiate Student Loan Trust 2006-2 and SMB Private Education Loan Trust 2021-A, which borrower defendants may not recognize as related to their private student loan.

Private student loan debt collectors use the courts to collect on defaulted debt. Like other unsecured creditors, they must file a lawsuit and obtain a court judgment before they can engage in involuntary collection such as wage garnishment and bank account levies. Private student loan debt collectors collecting against California residents have four years from the date of the breach of contract, or the date of the last item on the account, to sue to collect a debt. This means that the right to sue expires after four years unless the consumer makes a new payment on the loan. Private student loan collectors often require a nominal $50 payment to be placed into forbearance, resetting this four-year clock.

Private Student Loan Borrowers Fare Poorly in Court

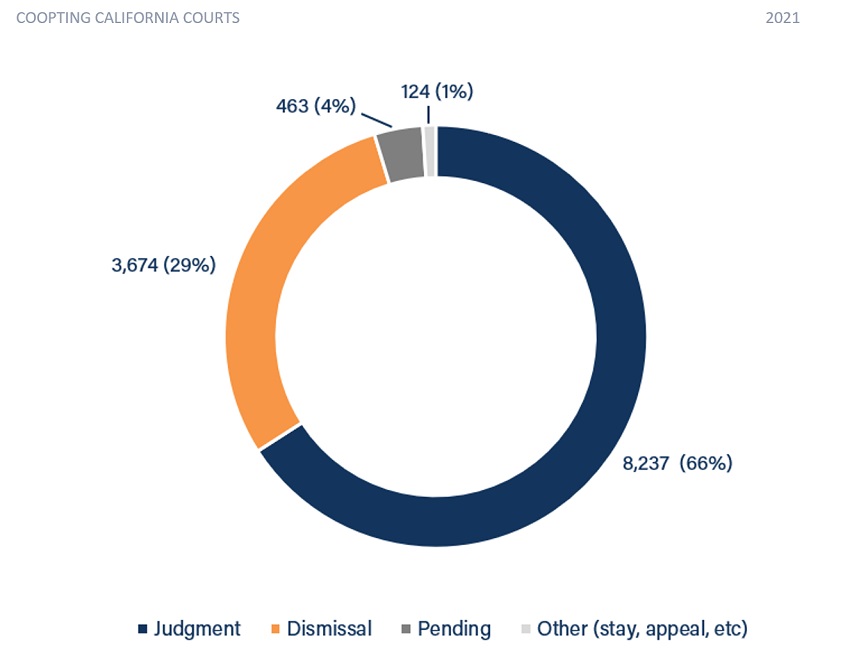

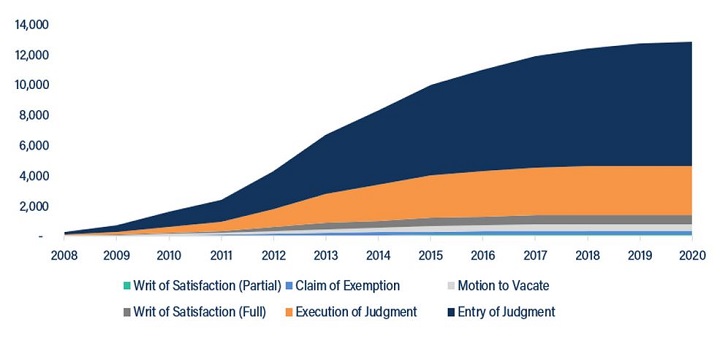

Findings show that private student borrowers who cannot pay their bills do not fare well in court. The rate at which student loan debt collectors win their cases is astronomically high. More than 66 percent of cases resulted in judgment against the borrower. This compares to debt collection cases in general in California, in which about 55 percent of cases result in a judgment. The data from the courts does not show why a case is dismissed, but settlement of a lawsuit is one way to avoid a judgment, and it may be that student loan borrowers have less success than other debtors in being able to negotiate an affordable payment plan that will allow them to avoid a judgment. Once a judgment is entered, analysis of the court data shows that few borrowers pay off the debt, facing wage garnishment and bank levies by creditors.

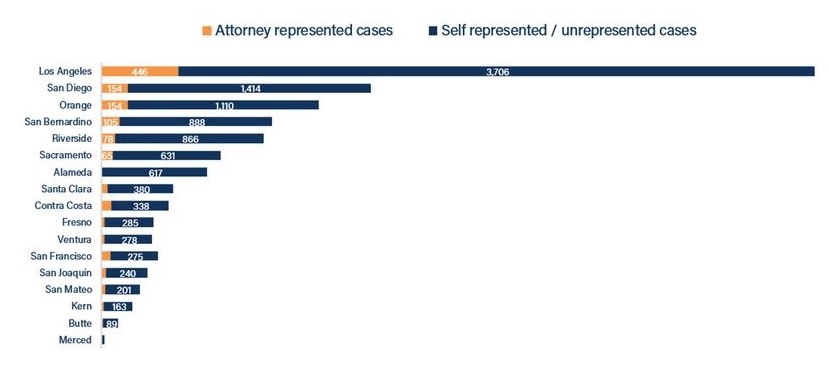

The data on default rates shows that many borrowers fail to file the initial paperwork required to dispute the creditor’s claim even though there are widespread and well-known evidentiary problems with the paperwork filed by high-volume student loan collectors. The court data also shows that borrowers are often on their own, without help to respond to legal paperwork. The study found that statewide, only ten percent of borrowers were represented by an attorney. This number drops to six percent or lower in some counties, such as Alameda, Fresno, and Ventura.

Analysis of post-judgment collection activity on California student loan debt collection cases shows that only 624 borrowers, of 12,499 cases analyzed, showed a “satisfaction of judgment” had been filed, meaning that the borrower had paid off their debt in full. This means that for the thousands of other California student loan borrowers whose debts have been turned into judgments, the debt balance will continue to grow at a rate of ten percent per year. The post-judgment activity analysis shows that 92.5 percent of judgments entered remain outstanding and collectible. The remaining executions of judgments were returned unpaid, either because the borrower earned too little money to garnish or because they were not receiving earned income at all.

California’s system of renewable judgments, with statutory ten percent interest accruing each year, burdens the most vulnerable student loan borrowers with an inescapable debt. A conclusion that may be drawn from these findings is that borrowers are not defaulting because they are choosing to stop paying on their private student loans. Among student loan debt collection defendants who are unable to pay their loans, borrowers overwhelmingly simply do not have the money to pay off their debts before or after the collection process proceeds through the courts.

California Should Take Additional Steps to Protect Borrowers

The California Legislature recently passed Assembly Bill 424, the Private Student Loan Collections Reform Act, which takes steps to improve outcomes for borrowers sued on student loan debts. This new state law, which takes effect January 1, 2022, will require that a student loan debt collector prove it has the right to collect a debt and places a higher evidentiary burden on the collector. It also gives borrowers the right to hold abusive creditors accountable and extends the time that a borrower can bring a motion to set aside a default judgment. This legislative change will provide relief for some debtors, particularly those facing newly filed lawsuits, but for many thousands of California consumers with old outstanding debt collection judgments, the cost of a few years of education continues to grow.

California should consider stopping this accrual of harm by reducing the interest rate for judgments and allowing judgments to expire on their own after ten years. New York’s state legislature recently passed Senate Bill S5724A, which would reduce the interest rate on consumer debt judgments from nine percent to two percent. This bill, which would apply to new entries of judgment as well as unpaid post-entry interest on existing judgments, is on Governor Hochul’s desk awaiting signature. Along with moving to halt the indefinite renewal of judgments, Californians should similarly consider reducing the interest rate on consumer debt judgments. These actions would go a long way to remediate the harm of old, outstanding consumer debt judgments and provide delinquent student loan borrowers, who are disproportionately borrowers of color, with a fresh start.